KEY TAKEAWAYS

- Value stocks have come roaring back, but the resulting performance lift has varied substantially across value managers.

- A continuous and accurate focus on value can put investors in the best position to capture value premiums when they appear.

- The relative performance of Dimensional strategies during the recent bounce-back for value reflects a continued ability to deliver value when value delivers.

Value is an asset class, not an investment strategy. Identifying low relative price stocks is only one step toward designing and managing a value strategy; differences in managers’ implementation skill can lead to a wide range of outcomes experienced by value investors. Investors can evaluate these outcomes by assessing whether managers delivered what they said they would deliver. In the case of systematic value strategies, strong performance during periods when value stocks outperform signals an ability to capture value premiums when they appear.

A DIFFERENCE OF OPINION

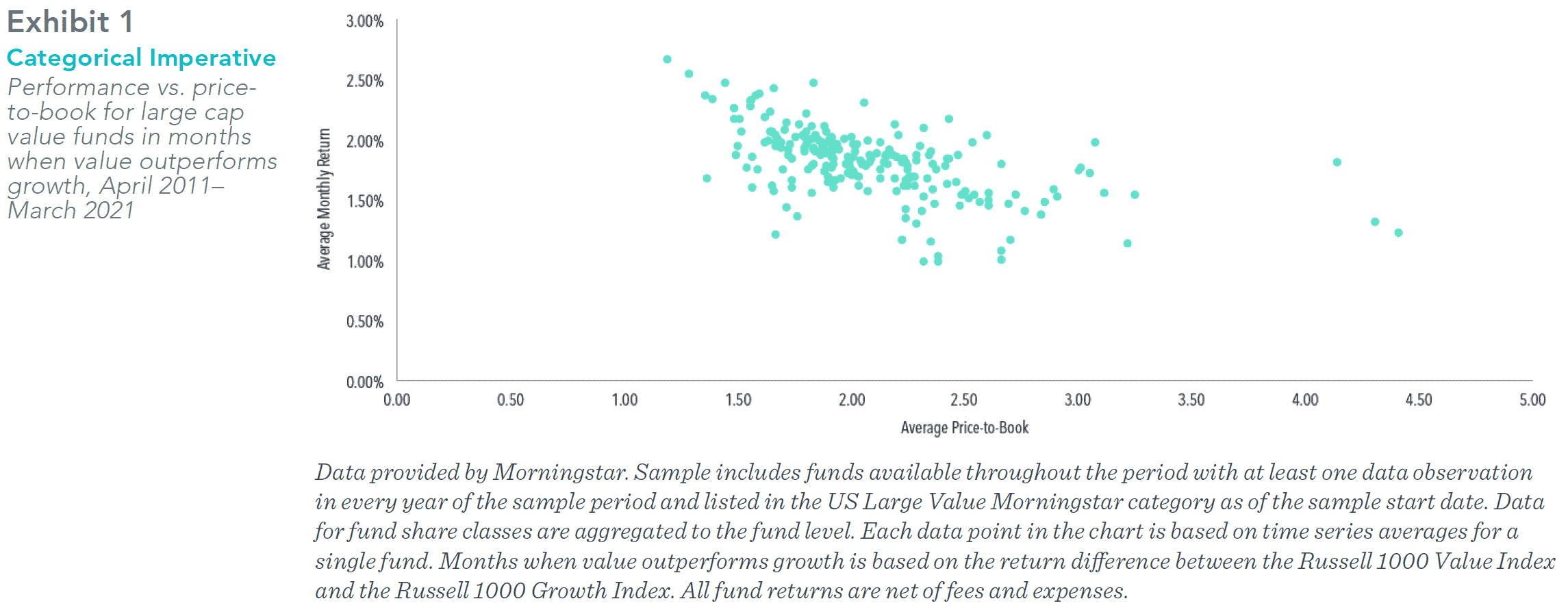

If 80% of success is just showing up, it follows that exposure to value stocks is a helpful start to capturing the value premium. However, even within a value category, exposure to low relative price stocks varies substantially across funds. For example, the 200-plus funds in the large cap value Morningstar category over the 10-year period ending March 31 had average price-to-book ratios ranging from 1.2 to nearly 4.5.That variation means not all funds in the category shared the same experience when the value premium appeared. In months when the Russell 1000 Value Index outperformed the Russell 1000 Growth Index, the average monthly net return for these funds ranged from 0.97% to 2.64%. A cursory inspection of the returns plotted against price-to-book ratios in Exhibit 1 reveals a negative relation for these months; all else equal, the greater the value exposure, the better the performance.

TESTING GROUNDS

Dimensional’s value strategies seek to maintain a consistent focus on value stocks, day in and day out. We do this because we expect a positive value premium every day. While realized premiums can be negative, there is no evidence investors can reliably predict such occurrences.1 On the other hand, there is ample evidence the value premium can show up in bunches.2 A process that stays the course in its pursuit of value can therefore boost the odds of harvesting the premium when value stocks outperform.

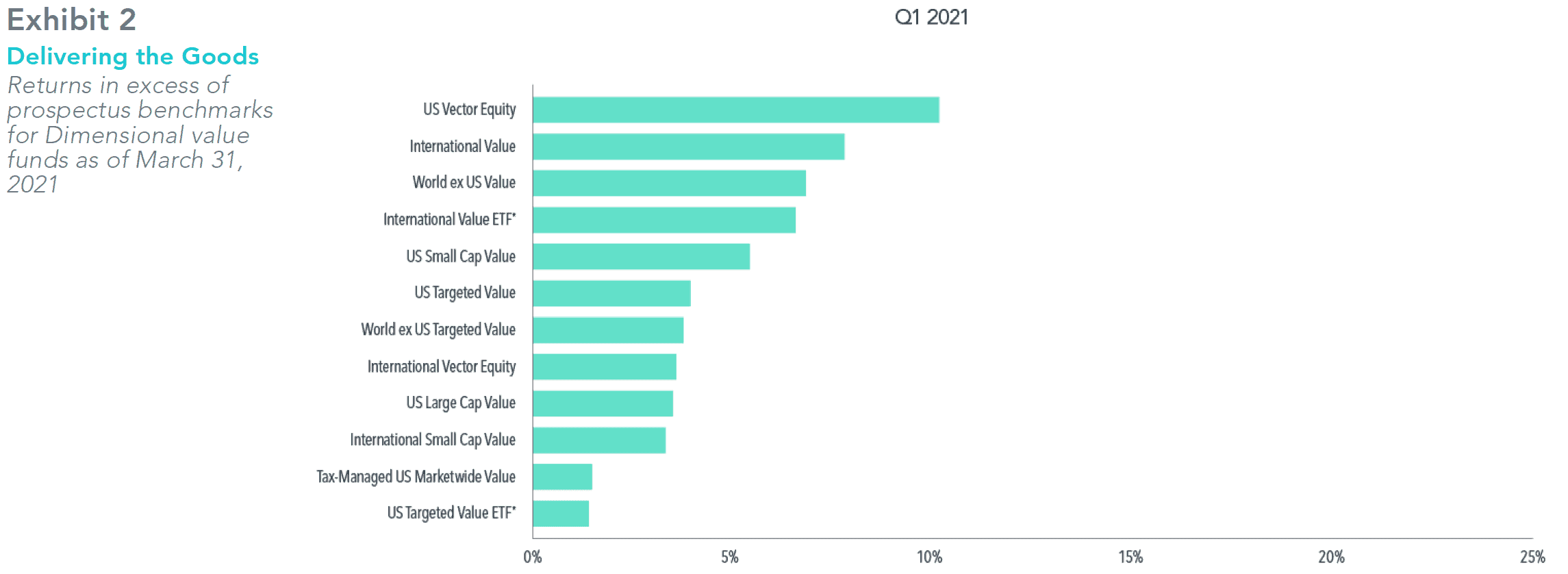

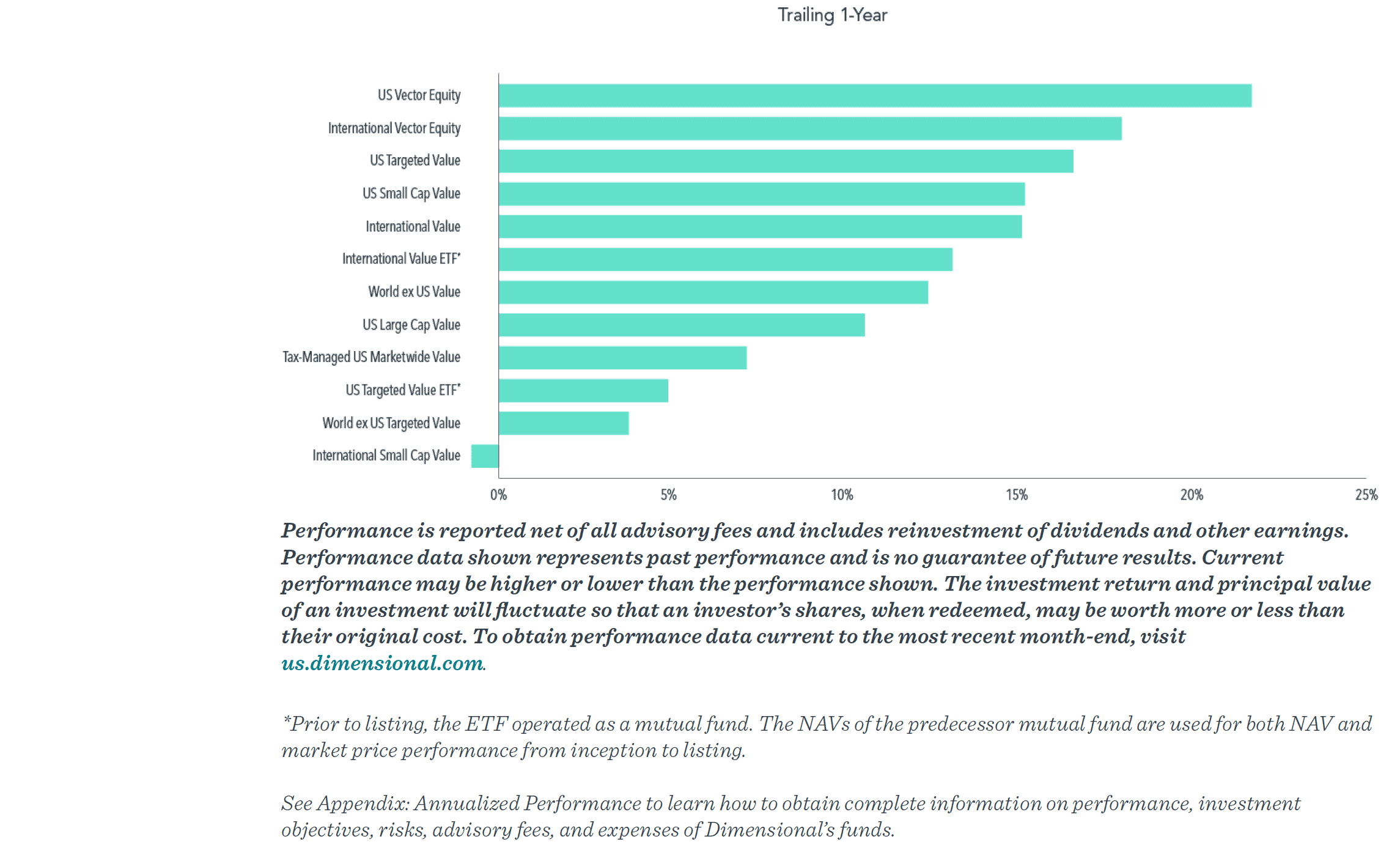

Strong recent returns of value stocks provide an opportunity to highlight the benefits of this approach through the lens of performance in periods of positive premiums. Exhibit 2 reports net returns for Dimensional value strategies in excess of benchmarks over both the first quarter of 2021 (when value stocks notably outperformed) and the 12 months ending March 31 (one year out from the 2020 equity market downturn). The results show pervasive outperformance across market segments and geographical regions. When evaluated this way, Dimensional’s value funds delivered on their goal of capturing value premiums when they appeared.

BUYER BEING AWARE

Even a period as short as one quarter can provide compelling evidence of whether managers delivered what they said they would deliver. And delivering on expectations helps investors pursue their goals by keeping the asset allocation decisions in their hands, not the manager’s. After all, uncertainty over what you’re going to get should be reserved for boxes of chocolates, not investment strategies.

1. Wei Dai, “Premium Timing with Valuation Ratios” (white paper, Dimensional Fund Advisors, March 2016).

2. “An Exceptional Value Premium,” Insights (blog), Dimensional Fund Advisors, October 2020.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Consider the investment objectives, risks, and charges and expenses of the Dimensional funds carefully before investing. For this and other information about the Dimensional funds, please read the prospectus carefully before investing. Prospectuses are available by calling Dimensional Fund Advisors collect at (512) 306-7400 or at us.dimensional.com. Dimensional funds are distributed by DFA Securities LLC.

This information is not meant to constitute investment advice, a recommendation of any securities product or investment strategy (including account type), or an offer of any services or products for sale, nor is it intended to provide a sufficient basis on which to make an investment decision. Investors should consult with a financial professional regarding their individual circumstances before making investment decisions.

Risks include loss of principal and fluctuating value. Investment value will fluctuate, and shares, when redeemed, may be worth more or less than original cost. Small and micro cap securities are subject to greater volatility than those in other asset categories. Value investing is subject to risk which may cause underperformance compared to other equity investment strategies. International and emerging markets investing involves special risks, such as currency fluctuation and political instability. Investing in emerging markets may accentuate these risks. The fund prospectuses contain more information about investment risks.

ETFs trade like stocks, fluctuate in market value and may trade either at a premium or discount to their net asset value. ETF shares trade at market price and are not individually redeemable with the issuing fund, other than in large share amounts called creation units. ETFs are subject to risk similar to those of stocks, including those regarding short-selling and margin account maintenance. Brokerage commissions and expenses will reduce returns.

09/20/2021

Expectations vs. Reality in Value Funds

KEY TAKEAWAYS

Value is an asset class, not an investment strategy. Identifying low relative price stocks is only one step toward designing and managing a value strategy; differences in managers’ implementation skill can lead to a wide range of outcomes experienced by value investors. Investors can evaluate these outcomes by assessing whether managers delivered what they said they would deliver. In the case of systematic value strategies, strong performance during periods when value stocks outperform signals an ability to capture value premiums when they appear.

A DIFFERENCE OF OPINION

If 80% of success is just showing up, it follows that exposure to value stocks is a helpful start to capturing the value premium. However, even within a value category, exposure to low relative price stocks varies substantially across funds. For example, the 200-plus funds in the large cap value Morningstar category over the 10-year period ending March 31 had average price-to-book ratios ranging from 1.2 to nearly 4.5.That variation means not all funds in the category shared the same experience when the value premium appeared. In months when the Russell 1000 Value Index outperformed the Russell 1000 Growth Index, the average monthly net return for these funds ranged from 0.97% to 2.64%. A cursory inspection of the returns plotted against price-to-book ratios in Exhibit 1 reveals a negative relation for these months; all else equal, the greater the value exposure, the better the performance.

TESTING GROUNDS

Dimensional’s value strategies seek to maintain a consistent focus on value stocks, day in and day out. We do this because we expect a positive value premium every day. While realized premiums can be negative, there is no evidence investors can reliably predict such occurrences.1 On the other hand, there is ample evidence the value premium can show up in bunches.2 A process that stays the course in its pursuit of value can therefore boost the odds of harvesting the premium when value stocks outperform.

Strong recent returns of value stocks provide an opportunity to highlight the benefits of this approach through the lens of performance in periods of positive premiums. Exhibit 2 reports net returns for Dimensional value strategies in excess of benchmarks over both the first quarter of 2021 (when value stocks notably outperformed) and the 12 months ending March 31 (one year out from the 2020 equity market downturn). The results show pervasive outperformance across market segments and geographical regions. When evaluated this way, Dimensional’s value funds delivered on their goal of capturing value premiums when they appeared.

BUYER BEING AWARE

Even a period as short as one quarter can provide compelling evidence of whether managers delivered what they said they would deliver. And delivering on expectations helps investors pursue their goals by keeping the asset allocation decisions in their hands, not the manager’s. After all, uncertainty over what you’re going to get should be reserved for boxes of chocolates, not investment strategies.

1. Wei Dai, “Premium Timing with Valuation Ratios” (white paper, Dimensional Fund Advisors, March 2016).

2. “An Exceptional Value Premium,” Insights (blog), Dimensional Fund Advisors, October 2020.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Consider the investment objectives, risks, and charges and expenses of the Dimensional funds carefully before investing. For this and other information about the Dimensional funds, please read the prospectus carefully before investing. Prospectuses are available by calling Dimensional Fund Advisors collect at (512) 306-7400 or at us.dimensional.com. Dimensional funds are distributed by DFA Securities LLC.

This information is not meant to constitute investment advice, a recommendation of any securities product or investment strategy (including account type), or an offer of any services or products for sale, nor is it intended to provide a sufficient basis on which to make an investment decision. Investors should consult with a financial professional regarding their individual circumstances before making investment decisions.

Risks include loss of principal and fluctuating value. Investment value will fluctuate, and shares, when redeemed, may be worth more or less than original cost. Small and micro cap securities are subject to greater volatility than those in other asset categories. Value investing is subject to risk which may cause underperformance compared to other equity investment strategies. International and emerging markets investing involves special risks, such as currency fluctuation and political instability. Investing in emerging markets may accentuate these risks. The fund prospectuses contain more information about investment risks.

ETFs trade like stocks, fluctuate in market value and may trade either at a premium or discount to their net asset value. ETF shares trade at market price and are not individually redeemable with the issuing fund, other than in large share amounts called creation units. ETFs are subject to risk similar to those of stocks, including those regarding short-selling and margin account maintenance. Brokerage commissions and expenses will reduce returns.

09/20/2021

Categories

Categories

Read Our Latest Articles Here

Michelle Maton Named to AdvisorHub’s 250 RIAs to Watch in 2026

High-Net-Worth Estate Planning Strategy: Flexibility and Generational Alignment

Dementia and Financial Planning: Protecting Your Family Before Capacity Changes